quantpylib.hft modelling

In the last post, we introduced our backtesting module:

The round-1 sign up for quant lecture demos on mid-frequency funding arbitrage are still open: https://t.co/mWUZE6sfBo

details are here: https://hangukquant.github.io/archives/QT410.pdf

We will reach out to those who have signed up, and subsequently determine if round 1 is closed.

To today’s post…

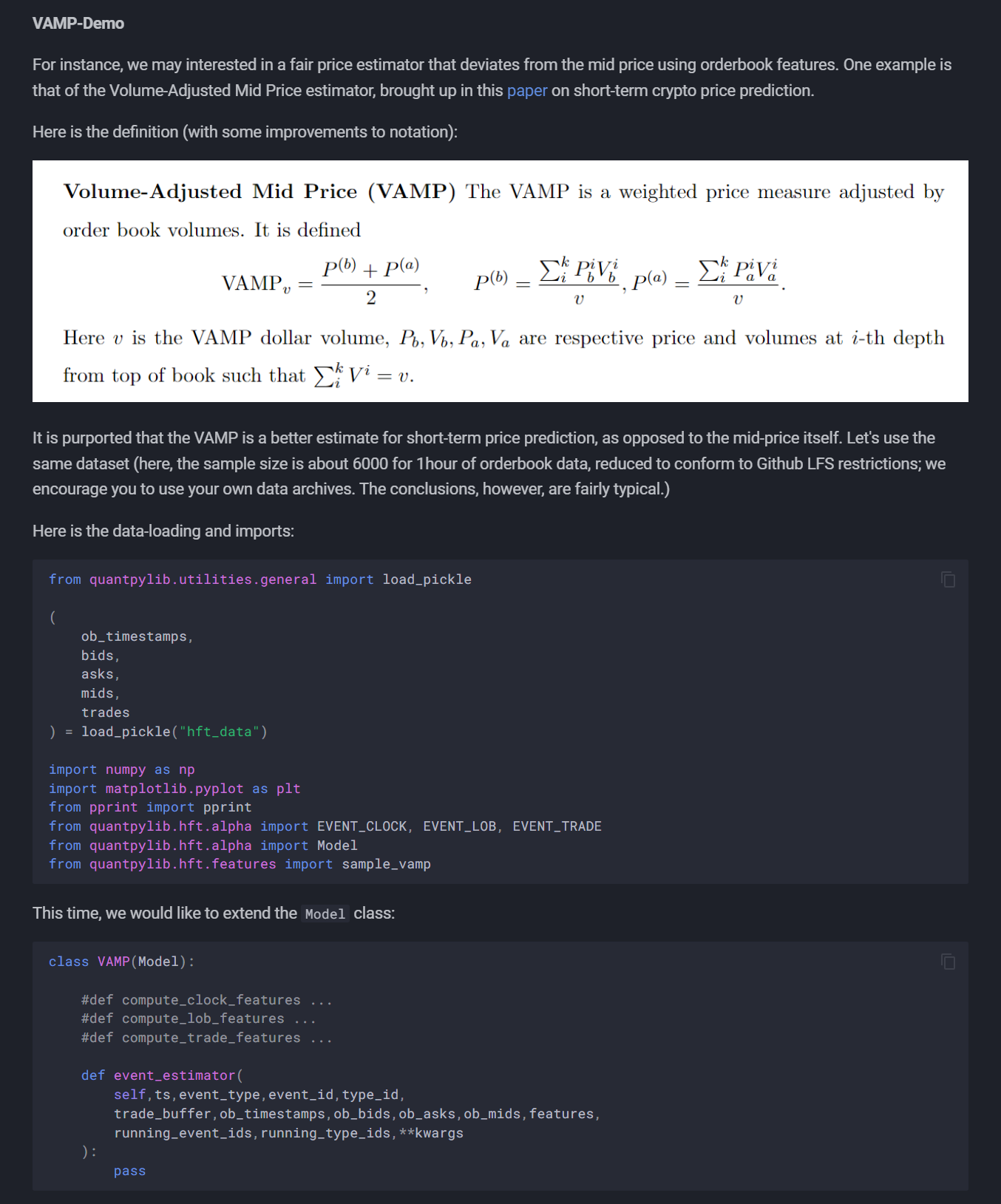

A sister module allows us to do hft modelling. In our example, we demonstrate the modeller by implementing the VAMP indicator (volume adjusted mid price) for this paper:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4351947

used for short-term price prediction. The results reflect that of the paper in terms of prediction error enhancements.

The full code demonstration is here, and the dataset is in the quantpylib/examples folder in the repo:

https://hangukquant.github.io/hft/hft/#statistics

The repo is intended for yearly subscribers (comment in this post):

preview…

When will the lecture be released on thinkfic for life time subscribers? :)