quantpylib.hft backtesting

anyhow, a short prelude: sign up forms for quant lecture demos on mid-frequency funding arbitrage are open:

this is the live pnl figure, y/x is ret/days. walkthrough on multi-instrument, multi-exchange, mid-frequency, maker-taker, perpetual-perpetual funding arbitrage bot implementation in binance-hyperliquid.

prereqs is just python programming. demo from scratch.

The details are here: https://hangukquant.github.io/archives/QT410.pdf

Last, we released our hpl library for seamless spot trading on quantpylib:

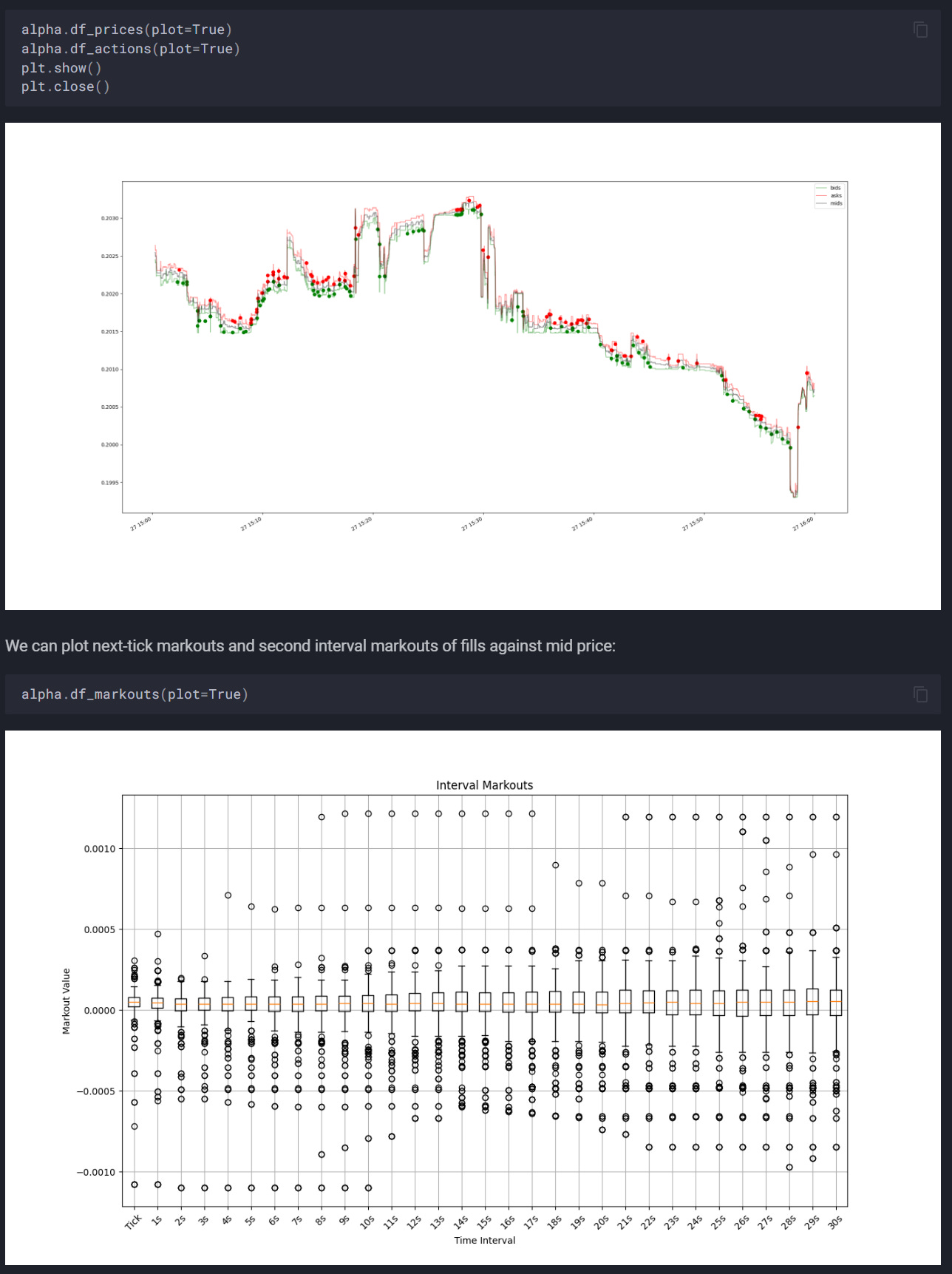

I am glad to release our hft backtesting library on quantpylib.

https://hangukquant.github.io/hft/hft/

There are active examples, demonstrations, and documentations up:

I have even included a mini dataset in the examples/ folder of the repo where you can play around with the dataset and the code.

Should be an extremely interesting helpful and exciting addition to the library;

the repo access is for annual readers, if you do not have access comment here: