Formulaic Alphas

In the previous post, we added on to the shrinkage methods and other optimization approaches to our backtesting library in the Russian Doll model.

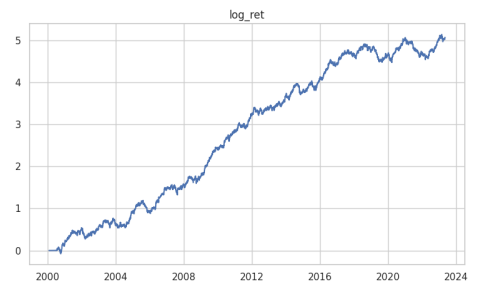

This week, we add on to our series on formulaic alpha trading. Here is the preview of the equity curve (net of zero fees):

The next week, we will skip the formulaic alpha report and instead release a special post to document the interpretations for the functions and primitives used in the alpha report. Additionally, in the upcoming posts, we will wrap up our discussion on stochastic calculus with the introduction of jump processes. The following week will see a continuation of the discussion on portfolio management and portfolio theory. We also intend to further deepen our discussion on linear algebra methods introduced thus far.

Formulaic Alpha report (paid):