Updates to quantpylib and some announcements

Updates to quantpylib and some announcements

A few days ago, we announced the quantpylib.thottler module:

enabling rate-limiting to native Python methods through a semaphore-like synchronisation tool utilising threads and coroutines.

Since, then we have adopted the semaphore to throttle requests on the datapoller, as well as added some more support on the decorator side for synchronous transactions. The relevant Github PR is here, and over coming days we will create example scripts and documentation:

https://github.com/hangukquant/quantpylib/pull/51/files

I have received comment that the recent posts have upped in difficulty, particularly w.r.t to the data library architecture. I am in the midst of creating lecture series on working with decorators, locks, conditions, asyncio, aiohttp, APIs, websockets, REST protocols - in relation to creating a data retrieval SDK for financial data. This would walk you through more advanced Python concepts.

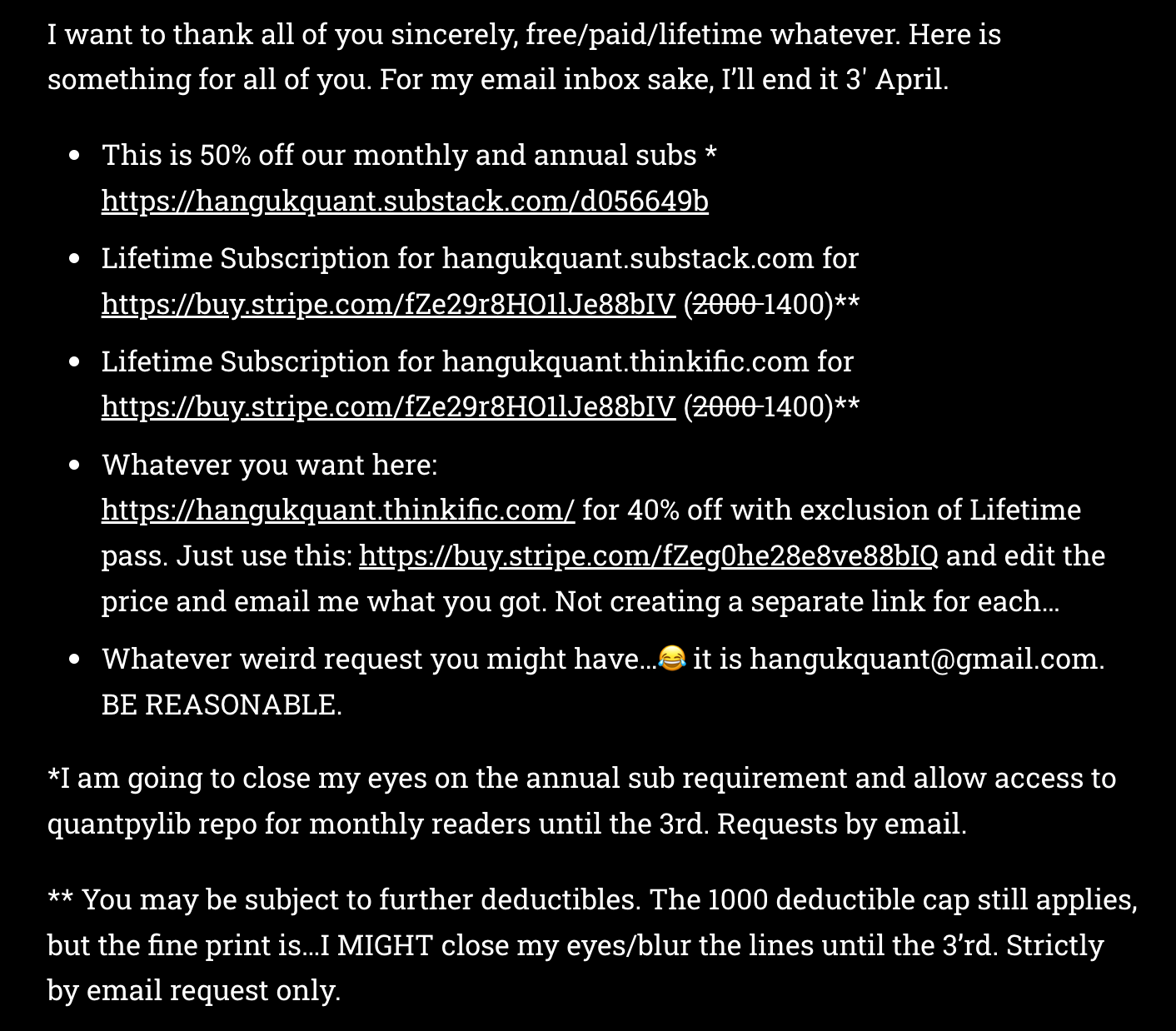

A reminder that we are running celebratory discounts on our content:

—» here is a preview of the available options. If you need to pay in crypto, please email me separately.

«—