quantpylib.hft.feed

Well there is some discount going on (left a few days) so do get on board if ya don’t have a quantpylib access yet:

any oh the how, I have improved the binance and hyperliquid wrappers, and also created the market data feed, docs and examples!

Let me show you exactly how simple it is to use, and how flexible it is.

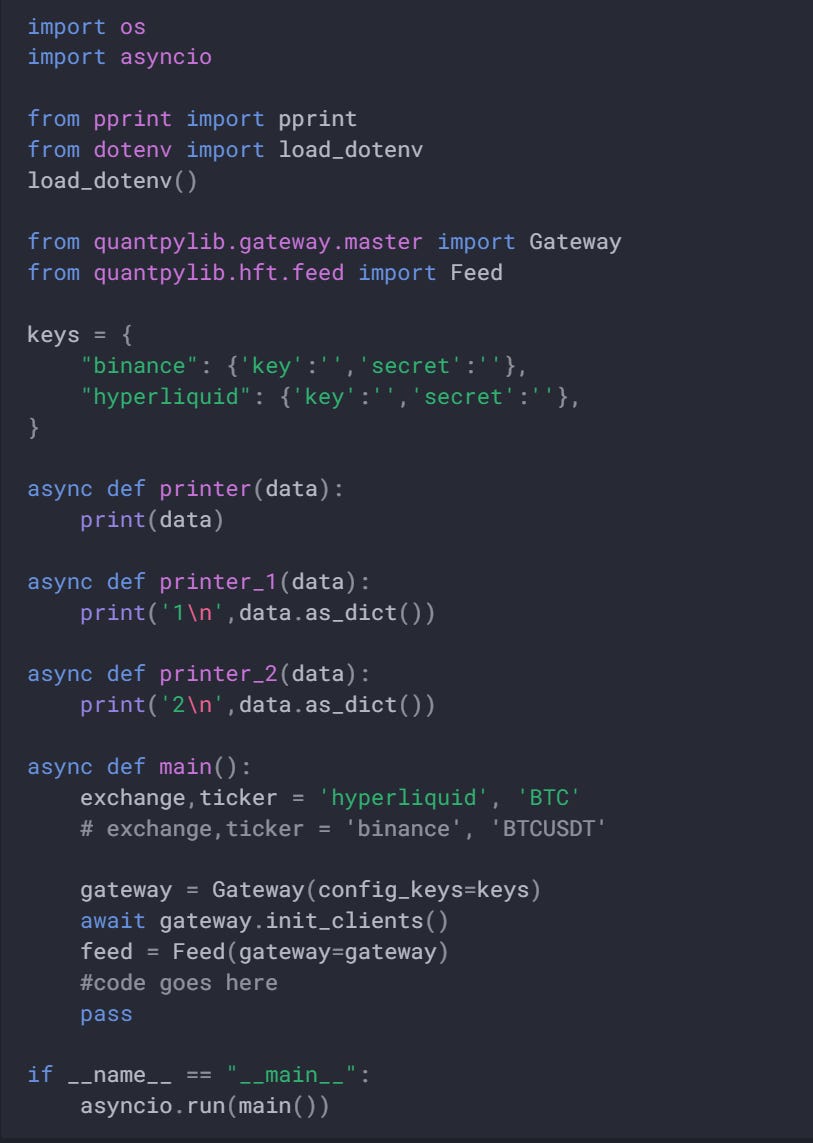

yada yada create your gateway object with keys, pass into feed:

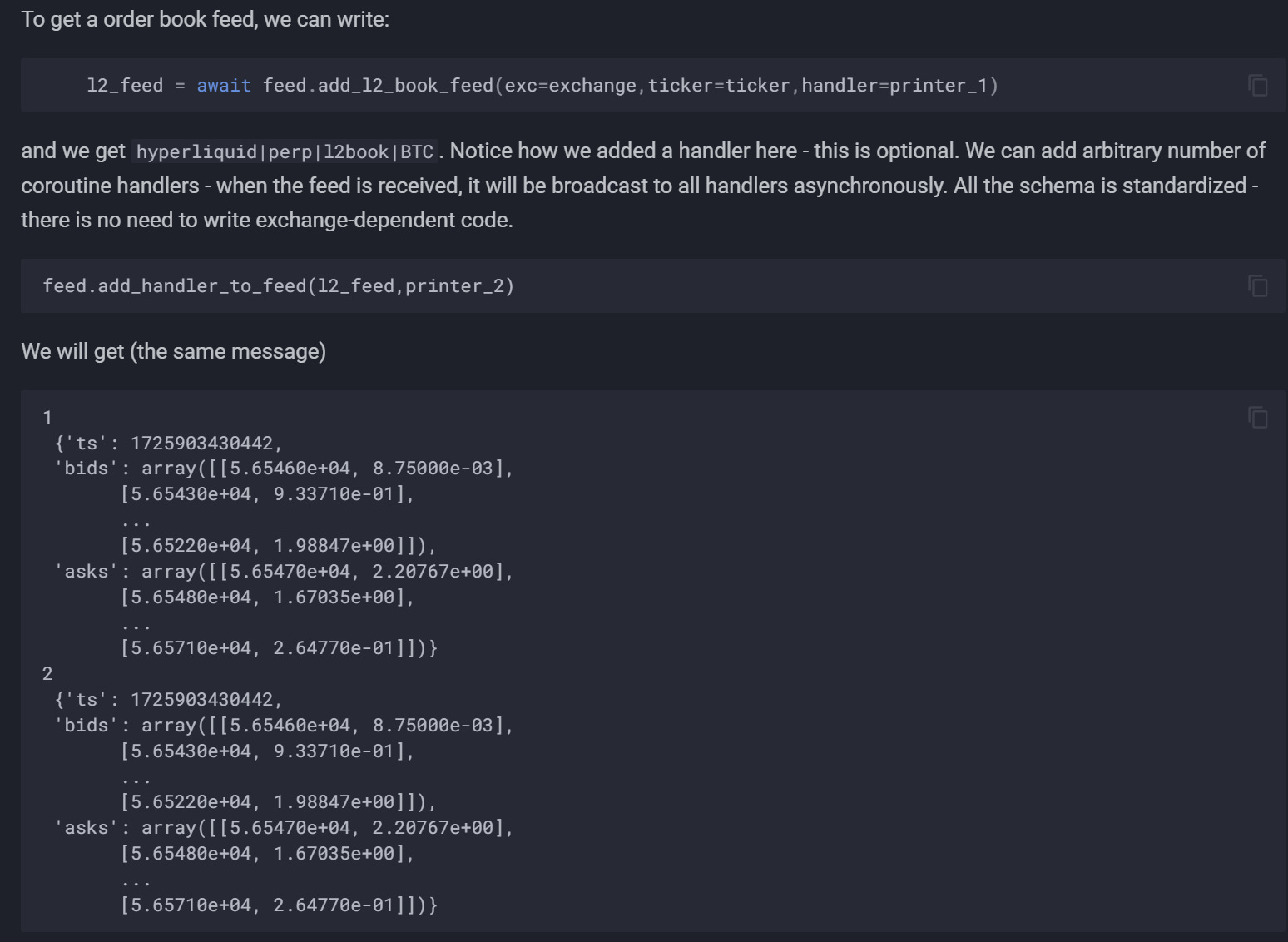

Add any number of handlers you want, at any point in the subscription. The feed will just start broadcasting the messages to the registered handlers:

Message is constructed from order-book delta updates - it is a local order book state. We can also control the depth of the streams, speed of update and how much data buffer we keep. In fact, using the feed ID, you can get our Order Book class which gives useful features:

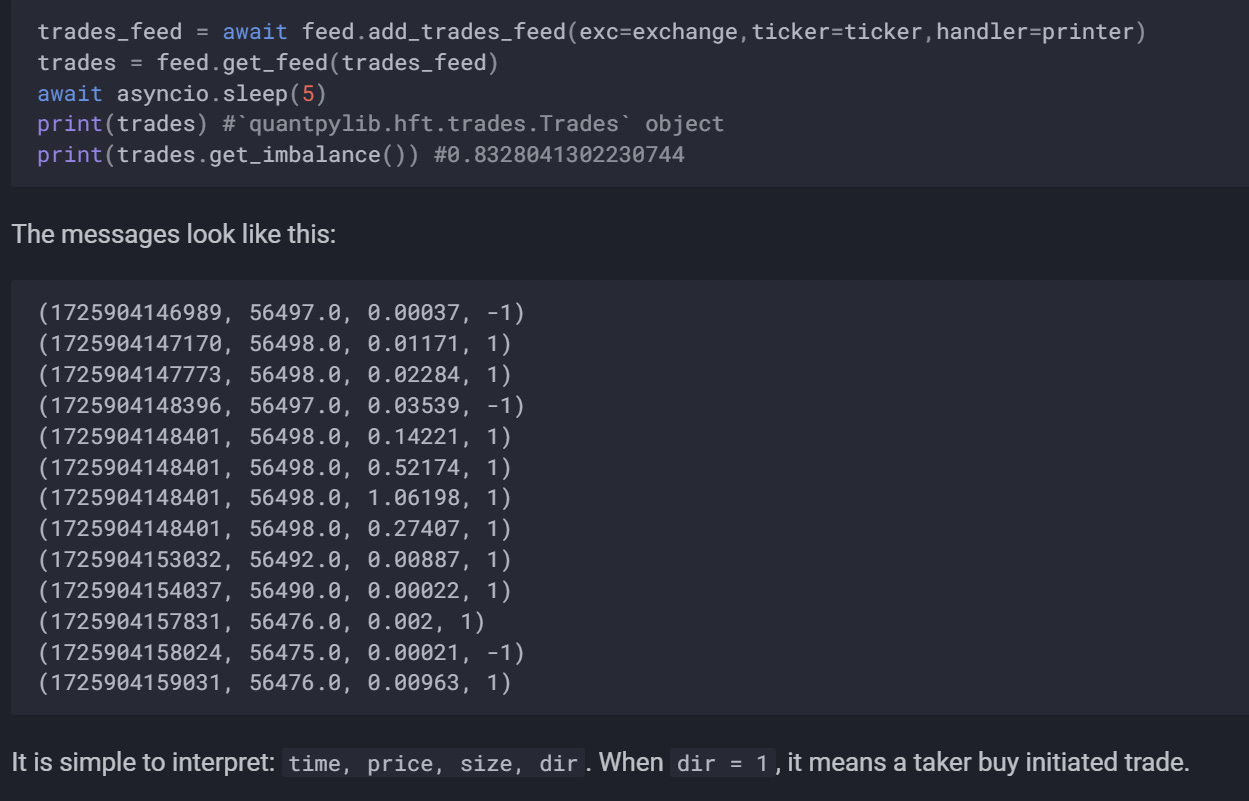

We can get the time-series of bids, most recent mid-price, bba, vamp indicators and what not from this object.

Same with trade feed, add any number of handlers, use the feed ID to get trades object and get order flow stats etc:

Quantpylib is Hangukquant’s student/trader Github Python library:

The docs is here: https://hangukquant.github.io/hft/feed/

The examples are here: https://hangukquant.github.io/hft/hft/#data-feed

Cheerios!