Market Maker v2 Script and the Open Research Standard

The deadline for the repo pass has finished, however - I didn’t quite have time to change the pricing yet, so the discounted repo pass is still open until probably some time tomorrow.

https://hangukquant.thinkific.com/courses/quantpylib

For those who signed up yesterday, I will add you guys after I close the discount access.

Since our post on the tick-data management:

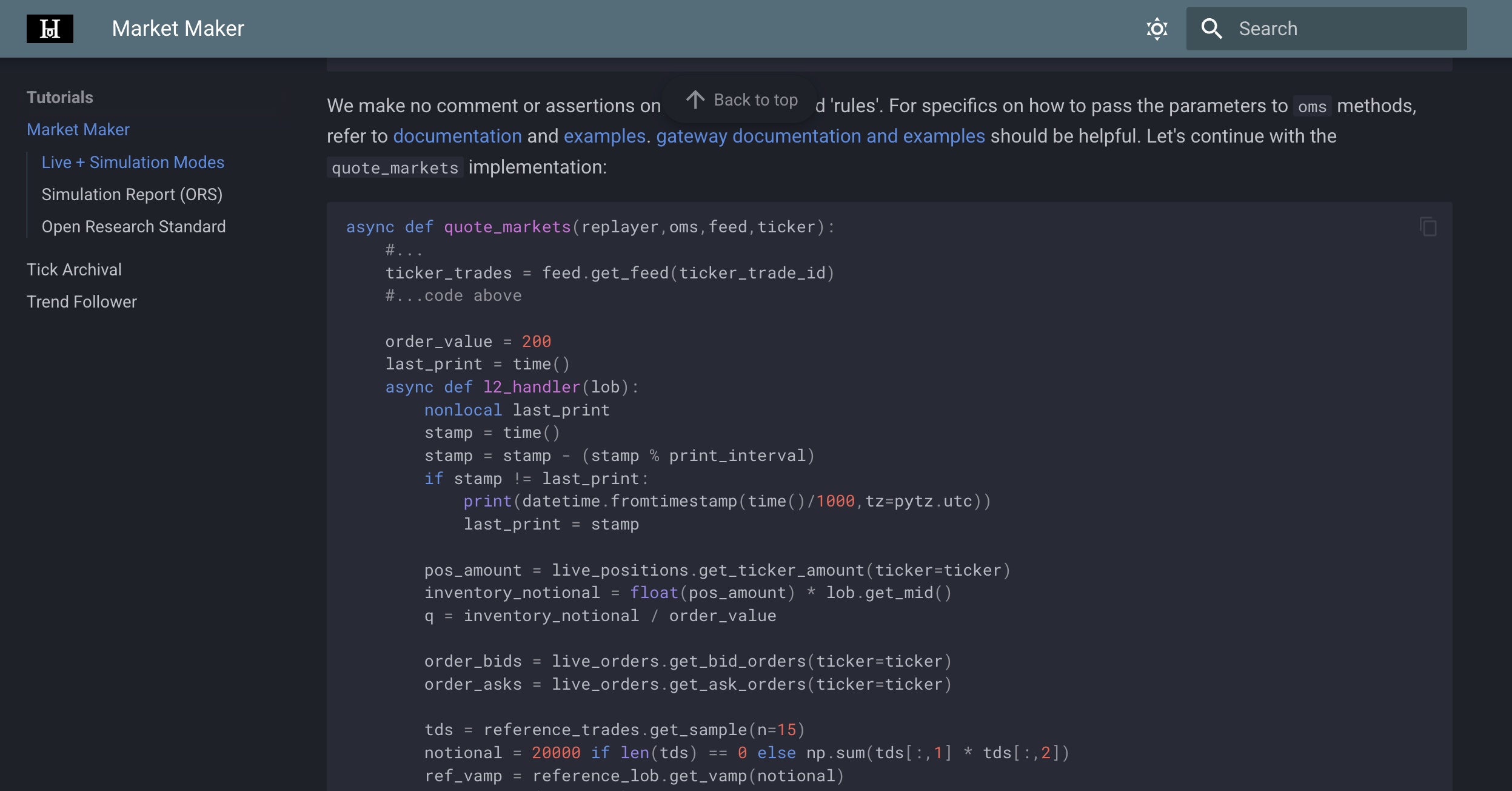

we have since revamped the market maker script and tick-data replayer. We have added some really useful plots, demonstrating how to do both backtesting and live trading with the quantpylib modules.

Additionally, we are pushing for Open Research Standard, quantpylib's push towards replicable, shareable and effortless quantitative research with code.

Quantitative research and papers are often extremely challenging to replicate either in part of the academic tendency for citation mining (lying with statistics) or variability in data, assumptions and implementation.

The ORS promotes reliable research with the automatic logging of code results, parameters and implementation.

See more here:

https://hangukquant.github.io/scripts/market_making/

The documentation is abit behind the tutorial, so in the coming days we will push up the updated documentation. Additionally, we will post new tutorials on tick-data modelling feature of the replayer class.