Big improvements to the market-maker backtests

Big improvements to the market-maker backtests

Last post,. we talked about the tick-data replay and simulator + mock classes for our trading agents:

There - we demonstrated how simple it is to perform an event-driven backtest starting from the market maker code. In fact, we wrote code such that a single boolean flag simulated=True/False gives us ability to switch between live trading logic and backtest logic.

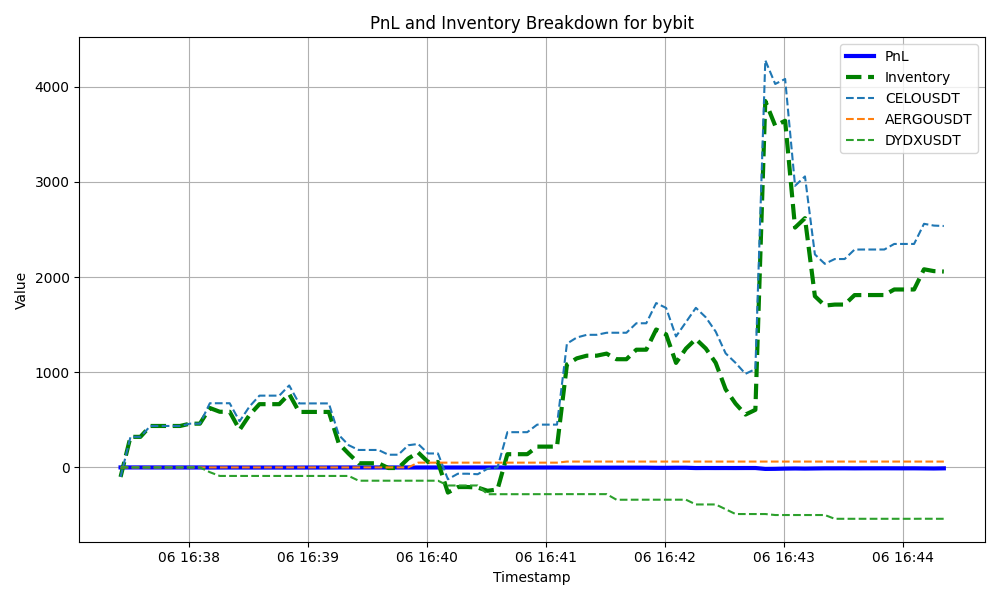

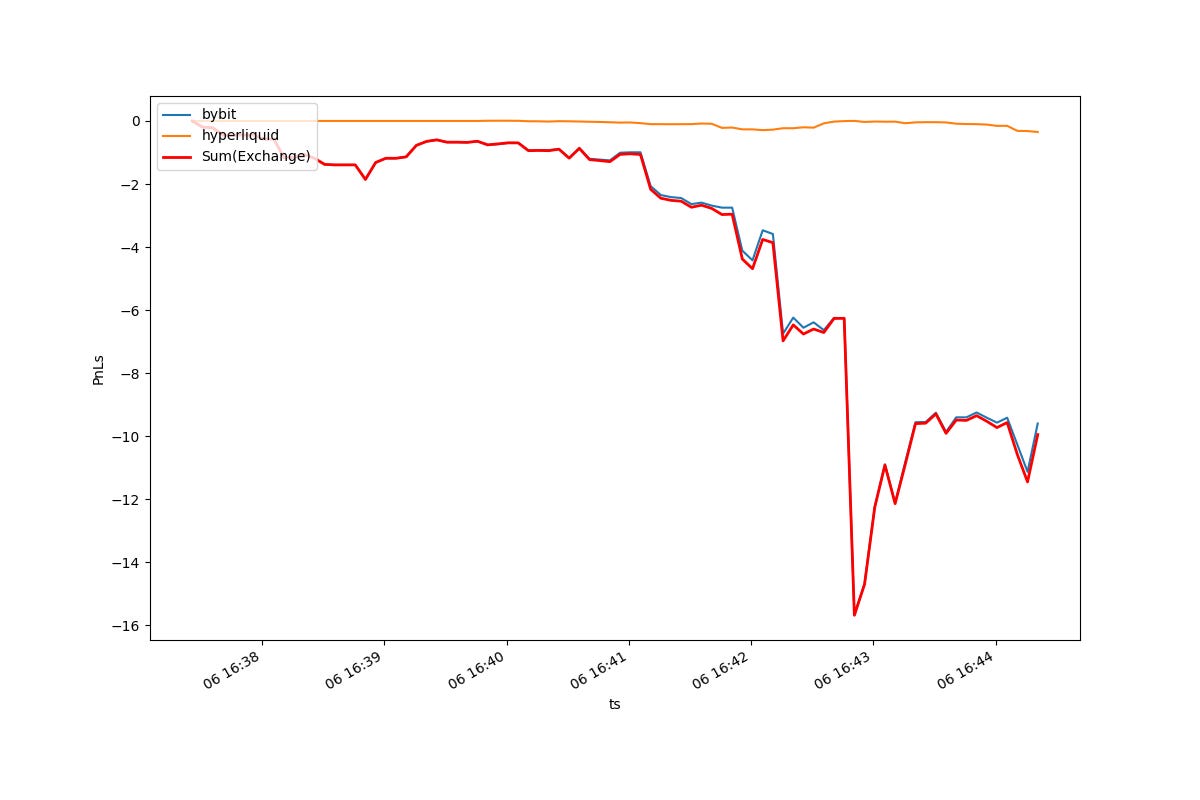

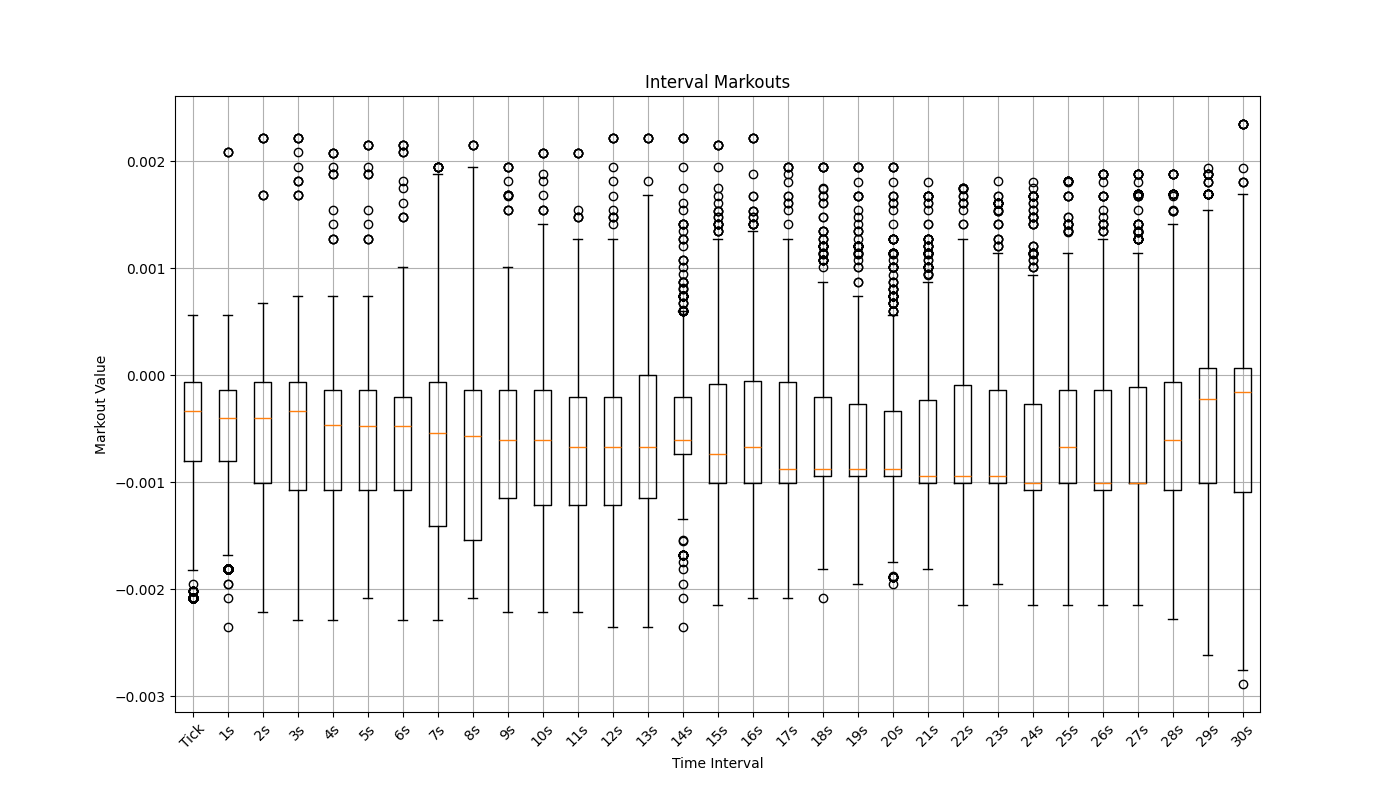

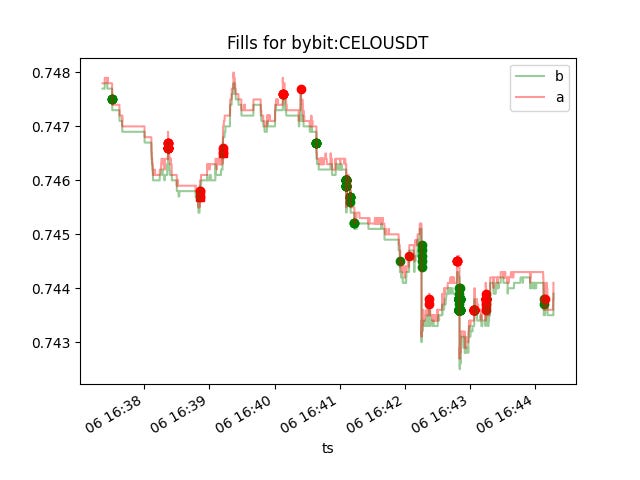

Since then, we have made big improvements, including accounting variable exchange maker/taker fees, added portfolio-exchange pnl graphics, exchange-inventory breakdown, markout plots, as well as clock-driven agents as supplementation to event-driven agents.

quantpylib is our community Github repo for annual readers:

Alternatively, you can get the lifetime repo pass:

https://hangukquant.thinkific.com/courses/quantpylib

The discount phase is over, but you can email me separately if you need financial aid. In the next post, we demonstrate how to utilize these new features, as well as configure our replayer class.

The full documentation for the new updates in this post are already pushed here:

https://hangukquant.github.io/hft/mocks/

with some preview graphics.

cheerios