Addition of the Oanda OHLCV and market data streaming to quantpylib

Addition of the Oanda OHLCV and market data streaming to quantpylib

In the last post, we added the notes on line profiling to the market notes.

Since then, there are a few updates. First, I would like to add that I created a YouTube account:

The QT101 lectures are now uploaded there. I am not sure how active of a public profile I intend to keep on there, but I might add a few video recordings and short quant notes/give previews to other quant lectures, so do subscribe. I would be very happy if you were to share the channel or just like the videos.

Additionally, I have implemented the Oanda REST API wrapper into the datapoller for the quantpylib Github repo. The details to join the repo is here, and is meant for annual/lifetime subscriptions:

The pull request is here:

https://github.com/hangukquant/quantpylib/pull/48

You can see that the development is rather quick…just 10 days ago, the datapoller did not exist, and now…we are looking at a fair amount of functionalities with Oanda, yfinance, eodhd, binance and phemex. We will continue to add more. Over the next few days, we are going to clean up the logic, and add a semaphore for throughput maximization on requests, so that the datapoller works at maximum throughput. We will also try to add documentation so that you can start to use the features.

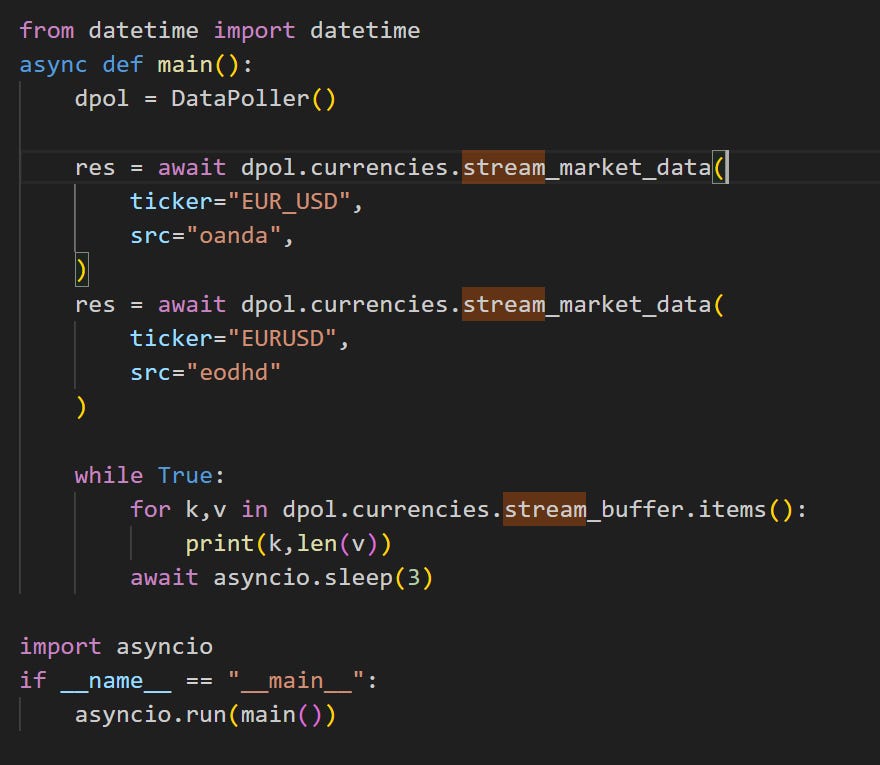

You can already see the huge improvement from the previous data master logic by how easy it is to interact with the poller APIs. Here is a cute example:

We will of course add documentation and sample scripts to demonstrate the full power of the data poller as we roll out the code and tests.